Inovayt Pty Ltd / ABN 25 126 141 982 / Australian Credit License 391333 / Inovayt Asset and Equipment Pty Ltd / ABN 57 658 320 248 / Inovayt Asset and Equipment is a credit representative of Fintelligence Pty Ltd / ABN 80 625 017 174 / Australian Credit Licence 511803 / Corporate Authorised Representative No. 539102 / Inovayt Wealth Pty Ltd / ABN 90 155 205 431 | Inovayt Wealth is an Authorised Representative of Alliance Wealth / ABN 93 161 007 / AFSL 449221 / Corporate Authorised Representative No. 435348 / All credit services are provided separately from Alliance Wealth, Alliance Wealth is not responsible for any credit services provided by Inovayt Pty Ltd and Inovayt Asset and Equipment Pty Ltd.

Client Login

Client Login

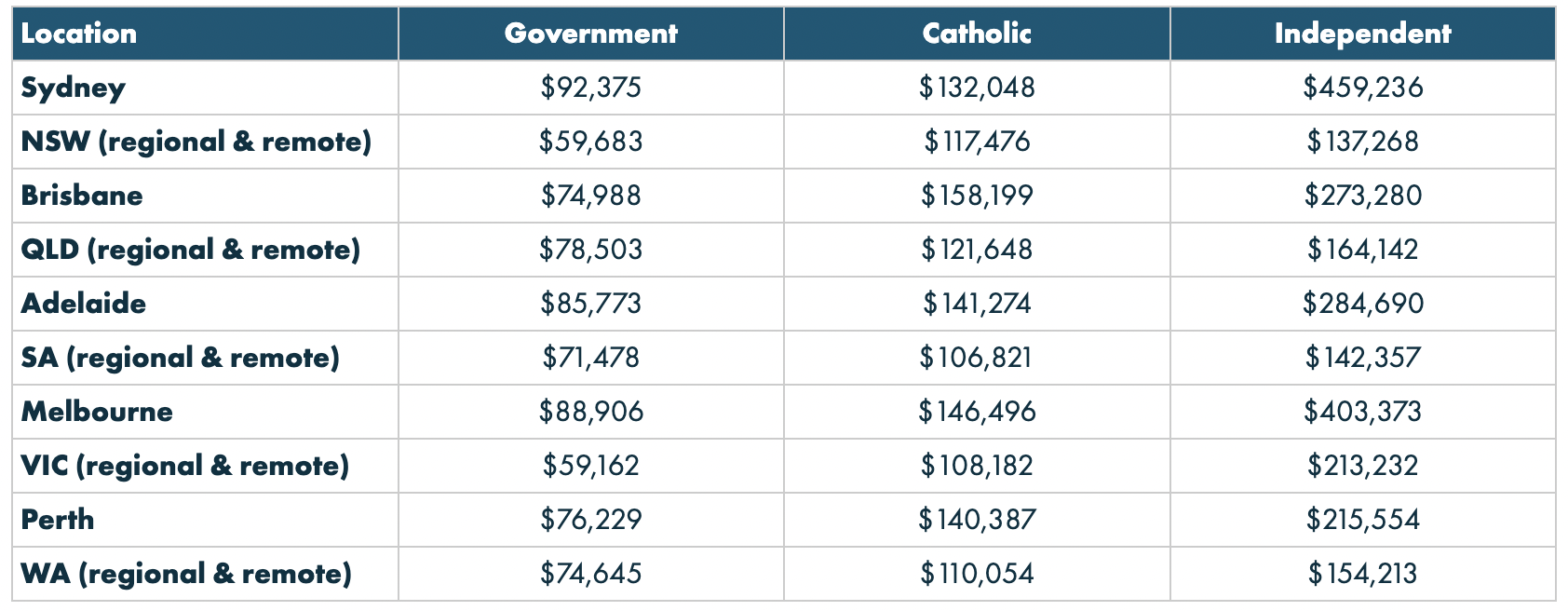

Source: Futurity

Source: Futurity